This week in ESG: Net Zero Banking Alliance members pull back from 1.5-degree goals; researchers urge better disclosures, quality grades for carbon credits

Sustainable finance

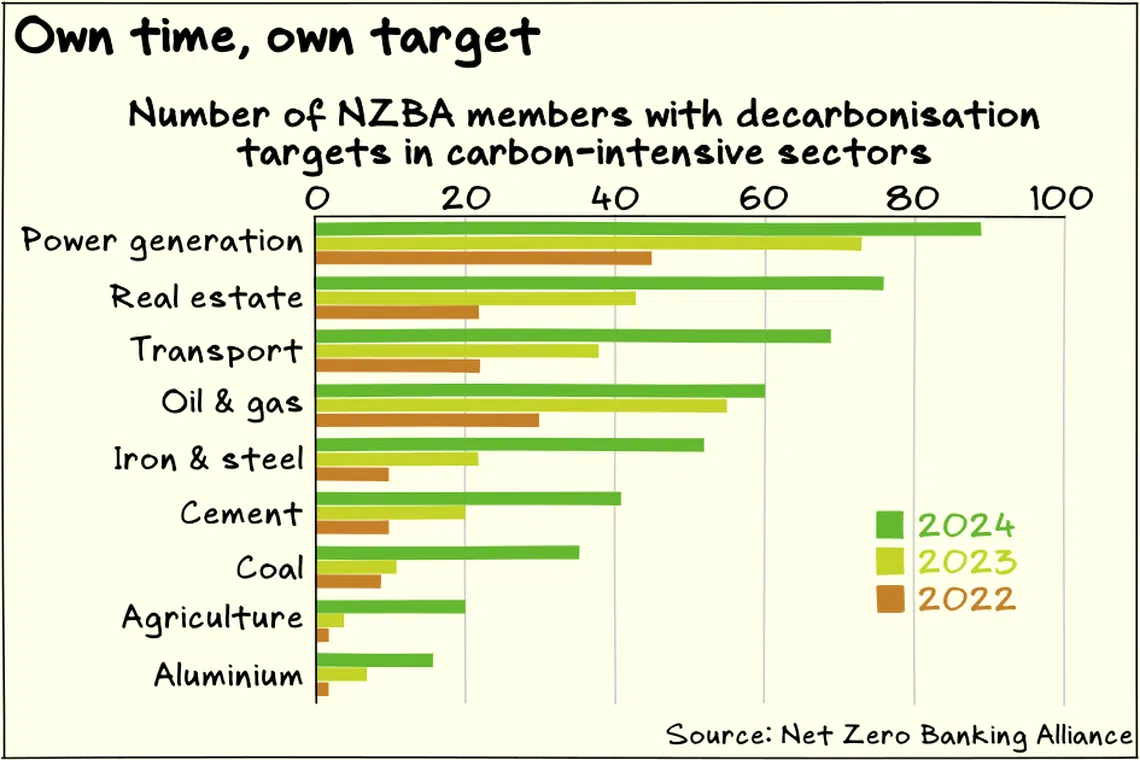

Banking targets watered down, but more honest

Let’s get one thing straight: Banks won’t save the world.

Members of the Net Zero Banking Alliance (NZBA) – a United Nations-convened industry grouping with more than 120 members – have just approved foundational changes to the NZBA’s ambitions. South-east Asia banks, including UOB and CIMB, were among those that supported the changes.

A NEWSLETTER FOR YOU

Friday, 12.30 pm

ESG Insights

An exclusive weekly report on the latest environmental, social and governance issues.

In newly revised guidance for the banking sector, member banks are no longer required to align their targets with pathways that limit global warming to 1.5 degrees Celsius above pre-industrial levels. Instead, the new goal is to limit warming to “well below” 2 deg C and “striving” for 1.5 deg C.

Member banks are also no longer required to aim for net-zero emissions by 2050. The new guidance does not mandate any timeframe.

The changes come as the alliance faces an existential threat after a number of banks – including US and Japanese lenders – have left the group.

The new changes give members considerably more flexibility to determine their own pace of decarbonisation. It will probably prevent more membership withdrawals from banks that did not think they could meet the previous targets.

There are two important takeaways.

The first is that banks did not think they could align the earlier, more ambitious net-zero targets with their profitability mission. Banks decide who they lend to, so in theory, imposing a 1.5-degree-aligned emissions condition is always possible. The reason that banks don’t do it is because they can’t make money that way. Unless everyone else has the same emissions test, a rejected client could simply find another financier, and the stricter bank would lose out.

The second takeaway is that banks do not think it is their role to set the pace of decarbonisation in their respective markets. Instead, they want that commitment to come from policymakers and industry consensus. The truth is that the banks’ net-zero commitments are substantially based on the banks’ assessments of how quickly decarbonisation will take place in the relevant sectors. There’s practically no additional decarbonisation impetus coming from the banks themselves. For example, Indonesia’s aim to reach net zero by 2060 is often cited as a reason why it’s not feasible for banks’ Indonesian portfolios to attain net zero by 2050. What’s typically left unsaid is that it’s not feasible to do so profitably.

As Mika Morse, a former climate policy adviser at the US Securities and Exchange Commission, wrote in a commentary that appeared in Responsible Investor: “Banks’ net-zero commitments were a mirage from the outset. The simple reason is that banks’ climate commitments rely heavily on assumptions about decarbonisation throughout the economy. They are fairly upfront about the fact that they were planning to reach net zero largely because they anticipated the entire economy would eventually reach net zero.”

The fundamental principle connecting those takeaways is that banks are businesses. Banks will align their portfolios with decarbonisation pathways only to the extent that it’s profitable to do so. That shouldn’t be a surprise, because banks are answerable to shareholders, who want to maximise returns on their investments.

The new NZBA goals mean banks can now have more pragmatic discussions about their decarbonisation strategies.

But just because a 1.5-degree pathway is no longer mandated doesn’t mean climate risk and opportunities have disappeared. Banks still require credible climate strategies, especially transition strategies, that adequately mitigate those risks and capture climate opportunities. And there’s still a lot of work that needs to go into aligning a portfolio to a less-than-2-deg-C pathway, even if that pathway isn’t as ambitious as before. Investors, especially those with longer-term horizons, will continue to demand transparency about those strategies.

A premium awaits banks that can demonstrate credible and ambitious climate and transition strategies. One downside of the lowered NZBA goals is that it lowers the barriers to pretender banks that aren’t abiding by the second part of the NZBA call on “striving” for 1.5 deg C. This raises the value of banks that can distinguish themselves.

The NZBA vote is also a timely reminder that policymakers need to step up. Waiting for the banking sector to come and save the day was never going to work out. But lending money and facilitating the flow of capital is an important part of addressing climate change, and banks play that critical role. Policies need to use the banking sector correctly, not as a pacesetter but as a force multiplier. Start with better policy support for sustainable financing, carbon pricing, research and development, and ambitious national and industry commitments, and aligned banks can multiply that impact across the economy.

Carbon credits

The need for better resolution

As Singapore continues to accumulate bilateral agreements to enable the partial offsetting of taxed emissions, the country could be increasingly exposed to reputational risk if emissions allowed into the country’s offset programme fail to deliver as promised, say researchers from the National University of Singapore’s Sustainable and Green Finance Institute.

Buying a carbon credit is an act of faith. Nobody actually delivers one tonne of carbon dioxide to your doorstep. The buyer has to trust that the amount of carbon dioxide claimed to have been removed or reduced was actually removed or reduced. To assure the integrity of the transaction, buyers rely on certification bodies to tell them which projects are trustworthy.

But current certification frameworks for carbon credits use broad categorisations of project types, which makes it difficult for buyers and project financiers to assess quality within those categorisations, the researchers say. The certification of certification frameworks by programmes such as the Integrity Council for the Voluntary Carbon Market and the Carbon Offsetting and Reduction Scheme for International Aviation makes the problem worse, ascribing quality based simply on who’s giving the certification.

The researchers suggest providing more detailed, relevant and standardised project-level data so that buyers and financiers can better determine the quality of each project. They also advocate for a shift away from broad pass/fail approaches and towards higher-resolution quality grades.

The researchers’ proposals reflect a broad trend towards treating carbon credits more like credit instruments with different levels of risk ratings. That’s a departure from earlier approaches that treated carbon credits more like commodities, where there is no difference between credits from different projects as long as they belong to the same broad class.

Risk ratings and better disclosures are helpful, especially when integrity is a fundamental problem throughout the carbon credit industry. Unfortunately, satisfying the need for better quality control inevitably leads to more costs for project developers. The challenge lies in striking a balance to address buyers’ concerns while maintaining a viable and efficient market for developers.

Other ESG reads

-

Temasek-backed ABC Impact finishes final close of second fund with more than US$600 million

-

Vietnam plans power exports to Singapore, Malaysia; boosts imports from Laos, China

-

China to tighten EV battery rules to reduce fire and explosion risks

-

Data centres in Asia must rethink cooling for a more responsible future